What is the worldly world users who are really thinking about Crypto and Web3 Banking? Dive into CROSSFI 2025 Survey

Crossfi dropped a bomb by scanning market research for 2025 – a sprawling study of more than 5,000 encryption users from India, Finland and Russia. This is not your model technology echo room. It is a live snapshot of the changing scene: 80 % of women, between the ages of 28 to 43 years, got $ 1,000 to $ 3,000 per month, and tend to cryptic currencies and Web3 banking services. Data challenges stereotypes, pain points, and future hints, where digital financing can compete with cash.

So, who leads this revolution? What hinders it? What should happen by 2025 to make encryption smooth like the dollar bill? Let’s think numbers, separate trends, and look at the future of money.

Survey in a glance: range and credibility

Crossfi has wiped 5,000 participants in three countries – India, Finland and Russia – supposedly, for their various economic and technological files. India is a hot point in India with the prosperous middle class; Finland, Commander of North Technology with high digital literacy; Russia is a wild card with a complex financial history. The participants were not random; They were users of encryption, probably through Crossfi or partnership platforms, giving the results a lens focused on the participating adopters. This is not a population poll; It is an encrypted and committed pulse examination.

Who uses Crypto? Demographic stood up

Heart of sex: Women take the initiative

Promise statistics? 80 % of the respondents of women, turn the scenario in the heavy past of males. Compare this to PEW Research of 2023, which found only 16 % of the United States encryption users were women. What leads this? In India, women-led financial inclusion programs-such as the government of Jan Dhan Yojana-may turn more women into digital assets. The culture of technology in Finland in Finland can be a worker, while Russia’s economic fluctuations may push women towards alternative wealth building tools. This is not a coincidence, it is a direction that begs for the deeper global research.

Age and income: the middle land

Most respondents decrease between 28 and 43 years, which is a sweet place to earn, save and invest. Their monthly income-from 1000 to 3000 dollars-with intermediate income arches in its areas, for all the data of the World Bank. In India, this is higher than the national average ($ 180 per month); In Finland, it is modest but it is suitable for living; In Russia, it is strong for urban professionals. Crypto is not only for billionaires or is not full – it resonates with the global middle class, a hungry financial control group.

Why this matters

This demographic mix is hinting on the expanded Crypto attractiveness. Women in these areas may see that it is empowering – a way to overcome traditional banking barriers. Meanwhile, medium income people may be seen as a hedge against inflation (5-6 % annually in India or instability in the currency (ruble ruble problems). It is no less than Lampus and more stability.

Crypting as a lifestyle: patterns of use and income

Hustle

Here is Kicker: Investment or Curled Currency Holding is the source of dominant income for respondents. Forget the daily trading or Meme-Coin-these users play the long game. This repeats the Foundelity 2024 report, with 52 % of institutional investors to coding growth. Bitcoin or etherum, and they hide it in governors, and their viewers (hope) climb. Some may share assets on platforms like Lido or lend to AAVE to obtain a negative income-harmful voltage strategies that suit their profile.

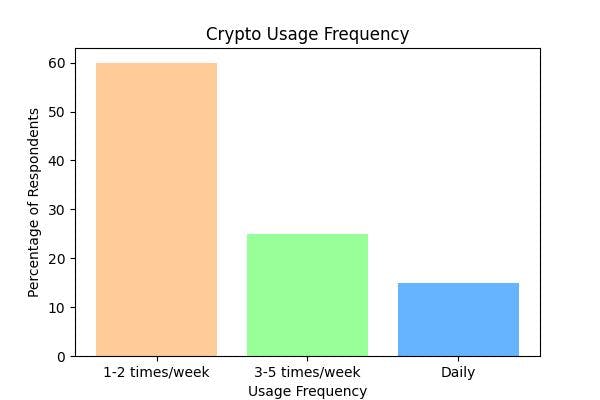

Weekly checks

Most of them deal with encryption from once to twice a week. What do they do? probably:

- Purchase: Decreases in stock exchanges such as Binance or Coinbase.

- Contract: Monitor the governor through applications such as the confidence portfolio.

- Earning: setting the assembly baths or claiming bonuses.

This is not the feverish pace for Wall Street. It is deliberate – like directing a digital garden. For medium -income users, it is a side bustle, and it is not a full -time disturbance.

Insight opened

This behavior indicates the development of encryption from the speculative game to the primary financial element. It is not a matter of noise “to the moon” – it is related to the construction of wealth gradually, especially in the areas where traditional investments (stocks, real estate) feel far -reaching.

Fees problem: The largest road barrier in Crypto

High cost pain

High transactions fees top the list of challenges – a global attraction. ETHEREUM gas fee increases once to $ 200 per transaction (ETHERSCAN, 2021), and as it reduces, there is still a blow from 10 to 20 dollars to someone who gets $ 1,000 per month. Bitcoin does not picn out – its climax at $ 60 in 2021 (Bitinfochars). For context, send $ 50 via PayPal costs. The encryption is not competitive yet.

Why do you bite the fees?

- Network congestion: ETHEREUM blockage during NFT mutations; Bitcoin is slow, depending on the design.

- Mining costs: work proof of work such as bitcoin energy, and upgrades up.

- No mediator savings: freedom of decentralization comes at a price.

Solutions on the horizon

- Layer 2 measurement: ribbed and ribbed ribs to cents.

- Faster chains: Solana and Avalanche process thousands of transactions per second, cheaply.

- Improving fees: Tools like Gasnow help user time transactions to reduce costs.

Risk

In order to reach a collective adoptive encryption, the fees must decrease. Fees worth 20 dollars for $ 5 coffee are other than Starter. The respondents’ frustration with a broader truth: The cost is the king in financial inclusion.

Web3 banking: The promise meets pain

What users want

Web3 banking- Financing that works with size, and decentralized financing-with capabilities: no banks, no limits, only you and your money. The respondents give priority to safety and reliability, and it is easy to know the reason. Traditional banks (Lyman Prades’ thought) fail or freeze (Russia’s 2022 sanctions). Web3 promise? Your assets, your rules – confirmed according to the code, not executives.

Check reality

However, satisfaction is light – most of them are “somewhat satisfied.” Why?

- Frozen accounts: Defi platforms can be closed due to errors (for example, Wormhole penetration of $ 320 million, 2023) or dehydration in liquidity.

- KYC Clashes: The regulations require “knowledge of your customer”, but decentralized systems flow in central identity centers. Download a passport on Blockchain? embarrassed.

Decoding the chapter

Web3 is unreliable freedom, but the bites of reality. KYC is a must – exchange like Binance to impose it, yet it resists Defi. Solutions such as decentralized identity (CIVIC, Selfkey) aims to bridge this, allowing users to prove identity without prejudice to privacy. Meanwhile, the frozen accounts reflect the lack of ripeness of Web3 – SMART contracts need audits, and users need to secure (think about Nexus Mutual).

2025 vision: encryption as daily criticism

The big dream

The respondents expect that by 2025, encryption will flow like Fiat. Imagine bitcoin hitting grocery or turning in Dogecoin – no delay, no noise. It is bold, but technology is attached to:

- Lightning Network: Bitcoin speeds to seconds, penny costs.

- Stablecoins: USDC and Tether Nix Polatility, dollars simulation.

- Payment bars: Solana Pay and Binance Pay Strateline Merchant Use.

Obstacles

- Volatility: even with stablecoins, frighten the wild sellers in Bitcoin.

- Adoption: Only 1 % of American merchants take encryption (PYMNTS, 2024).

- Rules: Taxes and RGS – Crypto’s Asset vary in the United States, currency in El Salvador.

What will take

- UX repair: spot apps like Venmo, not Clunky portfolios.

- Trader incentives: cash recovery in Crypto? Less fees than the visa?

- World Universal Reges: The European Union is a model – mothers must follow.

Safety first: Cyber security concerns looming on the horizon

The threat scene

Cyber safety and security dominates fears – for a good reason. The breakfast penetrated $ 1.7 billion in 2024 (chain). Special keys are different; The carpet pulls tank projects. Experiences such as FTX collapse. For every victory, there is a fraud.

User shield

- Devices Governor: Professor and Trezor notebook maintain their keys in non -communication mode – only 10 % use (Scanning 2023).

- Multi-Sig: It requires multiple approvals, frustrating thieves.

- Education: Discovery of fake or ICOS provides millions.

Industry reforms

- Best Ux: Biometric records recordings or social recovery (Argentine wallet).

- Insurance: Defi coverage from Unlashed or ENSURACE.

- Certik and Trail of Bits Catch Constrics.

Crossfi play: Dam two worlds

Crossfi is not only reporting – it’s construction. Their Crossfi series merges FIAT and Crypto with non-will technology-users carry the keys, but transactions feel smooth. Targeting women in India or middle -papers in Russia, chasing totalitarianism. It is a plan for 2025: encryption is practical, safe and open to all.

Big picture: What next?

Crossfi wiping is not fixed – it is a road map. Crypto and Web3 Banking rewrites the financing, but they are not ready for primitive time. Here is the playing book:

- Cutting fees: Class 2 and new chains should be expanded quickly.

- Ux simplification: hide Blockchain, show benefits.

- Security increase: easy -to -use tools that overcome breakthroughs.

- Coordination of rules: global clarity opens adoption.

Crypto raises his specialized skin, reaching ordinary people with big dreams. By 2025, it may only be delivered. Dive into the full report of Crossfi and see yourself – digital and important in the future.

Do not forget to love and share the story!

Detection of the acquired interest: This author is the publication of an independent shareholder across

is less than $ 5 now supports this trend 0.025 DEFI ALTCOIN")