Financial nihilism in crypto is over — It’s time to dream big again

|

For crypto fans who came of age during earlier eras — back when Bitcoin was going to bank the unbanked and stop all wars, or even during the ICO boom when tokenizing carbon credits and disrupting dentistry were touted as the future of finance — the last couple of years have been incredibly depressing.

On the one side, some Bitcoiners who used to want to smash the unfair financial and banking system now cheer the world’s biggest banks and governments for gobbling up an increasing percentage of the supply.

And on the other side, there’s the financial nihilism of memecoin trading, where nothing of value is built or created — just a production line designed to extract as much cash as possible from retail. The vast majority of Pump.fun users, 99.6%, haven’t even made $10,000 on the site.

Ethereum creator Vitalik Buterin has always believed crypto can make the world a better place but seemed to have a crisis of faith back in February about where the industry was headed.

“Do I feel good when I hear people from crypto twitter and VC firms telling me that PvP KOL degen casino that’s money-losing for >99% of its own users is the best product market fit that crypto is going to get, and it’s ‘condescending and elitist’ to wish for something better?” he asked.

So how did crypto lose its way, and does the industry need to rediscover idealism and big dreams to get its mojo back?

Peace, love and crypto’s anarcho-capitalists

Scott Melker, better known as the Wolf of All Streets, says the early days of crypto were infused with a much greater sense of purpose than today.

“Early cypherpunks were true libertarians who deeply believed that money and the government were broken and that Bitcoin and blockchain technology could fix them,” he tells Magazine.

Ethereum co-founder Joe Lubin says the beauty of Bitcoin and crypto in those early days was how it attracted “philosophically diverse” groups to imagine different possible futures using the tech, including “cypherpunks, crypto-anarchists, libertarians, hackers, leftists, anti-corporate activists, and even socialists.”

“It is a testament to the power of the technology that all of these philosophies saw elements of what they cared about in the decentralized protocol technology, because it was flexible enough and powerful enough to build anything on top of it.”

Bitfinex chief technology officer Paolo Ardoino says there are plenty of true believers still building in crypto, but idealism has been “overshadowed by speculation.”

“From the beginning, blockchain was about financial inclusion, self-sovereignty, and breaking free from the limitations of the traditional financial system. But as the market grew, speculation took center stage, and for many, crypto became just another casino rather than a tool for empowerment.”

The ICO era was 99% memes,

However, idealism and mercenary financial speculation have existed side by side throughout crypto’s history.

In many ways, the initial coin offering boom in 2018 foreshadowed the memecoin frenzy, given many projects were little more than a half-baked idea (or meme) spun into a white paper and presentation deck that earned millions.

It was often cynical and exploitative, with many ICO founders frittering the money away before they’d even built a minimal viable product. ICO mills sprung up to scour the internet for new founders, who they put in with market makers, exchanges and marketing agencies to generate new ICOs.

“They had a whole playbook, and they would launch the ICO and just spit them out the other side and take 10% of the tokens,” recalls Kain Warwick, who ran Australia’s most successful ICO, which turned into Synthetix. “Like 98%, 98% of ICOs were [scams].”

A 2018 study by Satis estimated that 81% of ICOs worth over $50 million were scams, while later research in 2022 from the University of Vaasa put the figure at 56.8%.

But the era did produce many quality projects that still lead the industry today, including Aave, Chainlink, Bancor, Polkadot, Tezos, Filecoin and even EOS, which is now known as Vaulta and run by its community.

“If you go back in time and stop ICOs from ever happening, the world’s a worse place,” says Warwick. “Did people lose money? Yes. Did a lot of grift happen and a lot of wastage? Yes, but we got so much good stuff out of it. Huge investments in infrastructure and DevEx (Developer Experience) and all of that stuff would not have happened without ICOs.”

Crypto idealism turns into ideology

Back in those days, everyone at least pretended to believe in crypto’s ideals of decentralization, banking the unbanked and creating a better world with blockchain.

Idealism is not without its own problems, however, and can quickly turn into ideology, characterized by narrow, prescriptive and exclusionary thinking.

Read also

Features

Charles Hoskinson, Cardano and Ethereum – for the record

Features

Crypto Pepes: What does the frog meme?

“When I got into the Ethereum space and started building, I definitely drank the Kool-Aid,” says Warwick, adding that DeFi Summer in 2020 was geared toward a niche audience that was “ideologically aligned with low barriers to entry, permissionlessness, censorship resistance, etc, and so if you were building a product, it had to adhere to those ideological constraints.”

Warwick reveals he was such an ideologue back then that he refused to allow Maker’s decentralized DAI stablecoin to be used in Synthetix because Maker had accepted the centralized stablecoin USDC as part of its collateral pool.

“We were insanely ideological, decentralization maxis,” he says. “And that held us back. It caused the project to really struggle.

“End-users don’t care about any of that. They want to use products that make their lives better.”

The rise of VC coins

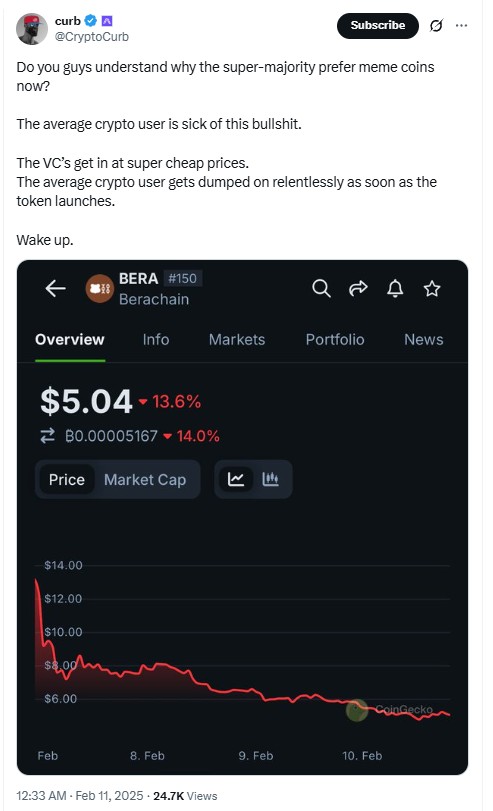

A big factor that turned the space toward financial nihilism was due to retail investors getting screwed by VCs on token launches.

“VCs have a lot of power and they restructured the game to make it maximally value extracted for themselves,” says Warwick

“Low float, high fully diluted value” became a common strategy from about 2020 onward. “Low float” refers to releasing just a small percentage of the total supply onto the market, which forces retail users to compete to buy the same handful of coins, pushing up prices.

“High FDV” refers to the total supply of the coin, much of it owned by VCs who’d drip-feed it back onto the market, killing token prices as the circulating supply grew ever larger.

A CoinGecko study found 21.3% of the top 300 cryptocurrencies are low float, high FDV, including projects like Celestia, Sui, Aptos, Injective and dYdX.

Eventually, retail speculators wised up to the fact the game was rigged against them and that they couldn’t win even by investing in quality projects.

“The reaction that they had was, ‘well, if I can’t play that game, this early-stage ICO-style game of buy a token really cheap and hope that it goes up, maybe I’ll play a different game.’ And the game that emerged out of that was memecoins.”

Memecoins were fair launches and offered the prospect of turning a few bucks into a few million. Nobody cared that the project and token didn’t actually do anything — as long as the price went up. It was the beginning of financial nihilism.

“People are naturally inclined toward gambling,” says Melker. “Most people come to crypto to get rich overnight, not to take a long time preference investment strategy into superior money.”

Financial nihilism: Speculation is everything

Lubin believes that people turn to memecoins because the system is broken. They watch as others amass huge wealth while they barely scrape by despite having a full-time job and college education.

“They feel as though cards are stacked against them and the game is rigged,” he says.

“Given this backdrop, it’s not hard to see why people turn to highly speculative assets that offer them a chance, however small, of making significant gains, and maybe even changing their fortunes.”

Read also

Features

The secret of pitching to male VCs: Female crypto founders blast off

Features

How do you DAO? Can DAOs scale and other burning questions

But for crypto believers and builders, the shift to memecoins left them feeling despondent. They thought they were building a generational change to the finance system, so it was a shock to find out users were as happy buying Fartcoin as Bitcoin.

“All of a sudden, everyone realized that the emperor had no clothes, that the speculators who were our users, who had been here for the last five years trying to get rich, didn’t care about any of the stuff that we cared about,” says Warwick.

“Now they were overplaying this memecoin game that has no utility, that is not developing anything, that’s not making the world better, that’s not ideologically aligned, it’s just a casino. And we’re like, Well, what the fuck is going on now? This is crazy.”

Memecoins jump the shark with Trump and Milei

Ironically, memecoins look as if they may have been killed by the same people who’d helped create them: mercenary grifters trying to extract as much money from retail as possible.

January saw the launch of the Donald Trump-themed memecoin TRUMP, followed two days later by the even more hastily thrown together cash-in MELANIA.

Chainalysis reported that around 810,000 wallets lost a collective $2 billion trading TRUMP, while $100 million in trading fees went to Trump’s companies, which control 80% of the supply.

The launch of the LIBRA memecoin a short time later — pumped by Argentine President Javier Milei — seemed like the final nail in the coffin. Insiders made a small fortune from the coin as it peaked at $4.5 billion in value before crashing 98%.

It’s too early to say memecoins are dead, but activity on Solana and Pump.fun has plunged in the aftermath. As with low float, high FDV coins, memecoins fans are realising the game is rigged against them.

“The problem is that the house always wins, and the game is much more fixed even than in a real casino,” says Melker.

Crypto idealism never died

Since the fall of FTX, memecoins have been the dominant narrative, if only because the SEC made it almost impossible to launch a project with real utility in the US.

Now that memecoin activity is dying down, crypto feels a little empty.

“You’re at a point now where it’s basically Bitcoin and financial nihilism at the two ends of the barbell and everything in the middle has suffered or languished,” says Melker.

“The idealism of earlier eras certainly still exists in the Bitcoin community, and in the ethos of many altcoins as well. With the embrace of Wall Street and governments, it is more important than ever that we educate people on the asset class, rather than allowing it to simply become another investment.”

Lubin points out that many builders and community members in Ethereum also remain true to the early spirit of crypto.

“The core tenets of that era and the people that were attracted to cryptocurrency at the beginning are still very much there. Maybe they’re hard to detect if you are outside due to layers of speculation, however, the most fundamental layers of the technology are still being built by people that genuinely care about decentralization.”

And while Trump’s tariff war may be weighing heavily on prices, the new pro-crypto SEC and the most pro-crypto government in Bitcoin’s history lay the groundwork for an explosion of new crypto projects with utility that deliver real value to the world, without having to worry about the legal risks of regulators stepping in.

Ardoino says the speculative memecoin era is drawing to a close.

“That phase is fading. The world is waking up to the fact that the traditional financial system isn’t just inefficient — it’s fundamentally unfair. Billions of people remain unbanked and even those inside the system are watching their purchasing power erode due to inflation, high fees and arbitrary restrictions. Crypto has always been about solving these problems, and now the focus is shifting back to real-world utility.”

He says the future of crypto is about delivering on the promise that crypto has always held.

“The next phase will be about building resilient financial infrastructure — one that operates outside the constraints of traditional systems and gives people true ownership over their assets.”

Subscribe

The most engaging reads in blockchain. Delivered once a

week.

Andrew Fenton

Based in Melbourne, Andrew Fenton is a journalist and editor covering cryptocurrency and blockchain. He has worked as a national entertainment writer for News Corp Australia, on SA Weekend as a film journalist, and at The Melbourne Weekly.