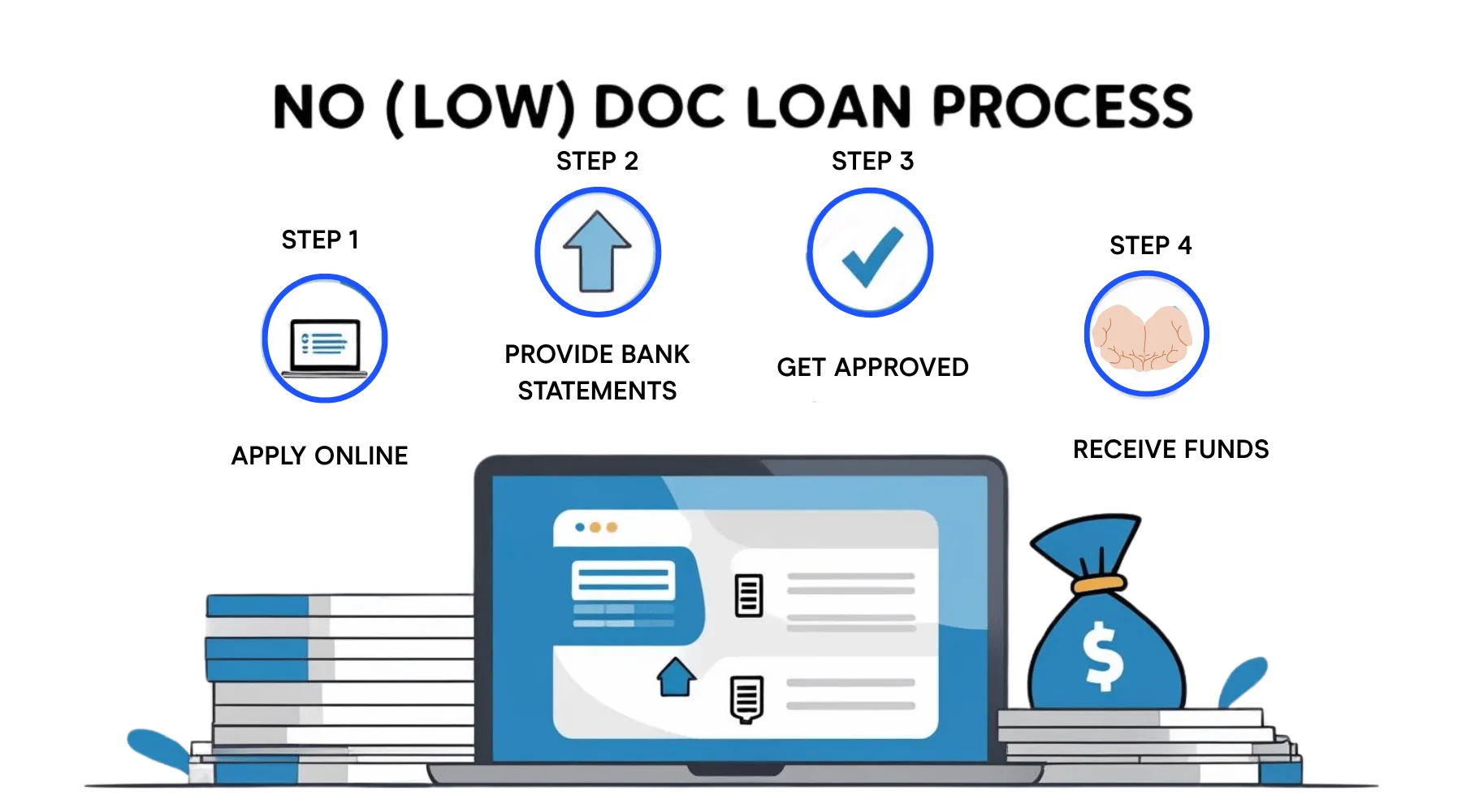

What is a no doc business loan?

A no doc business loan provides fast access to capital with minimal paperwork. Instead of tax returns or full financial statements, lenders evaluate your business using recent bank activity or revenue history. They’re designed for speed and simplicity, especially for borrowers who can’t produce standard paperwork or need to move quickly. These loans are faster to fund, but costlier and more restrictive in repayment terms.

- Minimal paperwork, faster access: No doc business loans offer quicker funding with fewer documentation requirements, relying instead on bank statements or revenue data.

- Higher costs, shorter terms: These loans often carry higher interest rates and faster repayment schedules, sometimes with daily or weekly payment structures.

- Best for specific needs: Ideal for startups, self-employed borrowers or businesses facing time-sensitive expenses, but less suitable for long-term capital needs.

What no doc business loans offer

No doc loans aren’t truly “documentation-free.” Lenders still need to assess risk. But instead of reviewing detailed financials, they may rely on bank statements, revenue history or collateral. The pitch is simple: faster funding with less scrutiny.

These products can be useful in a few situations:

- New businesses without established financials

- Self-employed borrowers with irregular income

- Owners prioritizing speed over cost

- Borrowers with poor or limited credit history

Who are no doc business loans good for?

Here are some examples of situations where a no doc loan may make sense:

- Startup founder. Needs $15,000 in emergency equipment repairs but hasn’t filed business taxes yet. Applies using three months of bank statements.

- Gig worker. Self-employed rideshare driver with seasonal income uses a low doc lender to smooth cash flow during slower months.

- Retail shop owner. Needs to pre-order holiday inventory but can’t wait for a traditional loan. Secures fast funding backed by POS data.

Expert insight: No doc loans are a lifeline — not a silver bullet

“We were in a fast-growth phase and needed capital to expand into new markets. A no-doc loan seemed like the quickest way to secure funding without getting bogged down in paperwork.

The process was fast. We filled out a short application, shared bank statements and got approved within a few days. The downside was the interest rate, it was higher than traditional loans and the repayment terms were strict. But for short-term needs, it worked.

We had explored traditional bank loans and also spoke with a few VCs. Banks were slow and wanted a ton of documents. The VCs were more focused on long-term equity deals, which didn’t fit what we needed at the time. That’s when we pivoted to no-doc options.

Watch the repayment terms and interest rates closely. A lot of them require daily or weekly payments, which can hit your cash flow hard. Also, make sure the lender is reputable — some in this space are not transparent about fees.”

Carl Jacobs

Cofounder & CEO of Apicbase

How to Qualify for No Doc Business Loans

No doc business loans offer more flexible eligibility criteria than traditional loans, but lenders still need enough data to assess repayment ability. Approval depends on alternative documentation and business performance, not tax returns or formal financial statements.

To improve your chances of qualifying, focus on the following:

- Consistent business revenue: Lenders typically want to see steady monthly income, even if they don’t require detailed financials. Expect to provide at least three to six months of recent bank statements.

- Time in business: Many lenders require a minimum of three to six months in operation, but some accept newer businesses if revenue is strong.

- Business bank account: Using a dedicated business account helps demonstrate cash flow and separate personal finances from business activity.

- Personal credit score: Not all lenders check credit, but a score above 600 can improve your approval odds and lower your cost of capital.

- Collateral or personal guarantee: Some lenders may ask for a personal guarantee, UCC lien, or business assets to secure the loan if documentation is limited.

Lenders prioritize speed and automation, so real-time access to your bank or sales platform data may be required as part of the application process.

Tradeoffs to consider

No doc loans are not a low-cost financing option. Lenders price in the added risk through higher interest rates and shorter repayment terms. Some may require daily or weekly payments. Others secure the loan against business assets or future receivables.

Pros

- Fast approval, often within 24 to 72 hours

- Minimal paperwork required

- Good fallback for borrowers with documentation gaps

- Options for startups and low-credit borrowers

Cons

- Higher rates than traditional business loans

- Shorter repayment windows (often under 12 months)

- Some lenders require daily payments

- May involve personal guarantees or collateral

Federal Reserve Business Lending Data for 2025

The 2025 Small Business Credit Survey (SBCS) reveals that 37% of small employer firms applied for a loan, line of credit, or merchant cash advance during the prior 12 months in 2023. Of these applicants, 50% sought $100,000 or less, and 30% applied for $50,000 or less. This data underscores the demand for smaller loan amounts, which are often associated with streamlined application processes and may include no doc loan options.

Who offers no doc business loans?

No doc business loans are typically offered by online lenders and alternative financing platforms. These providers specialize in fast decisions and revenue-based underwriting. Traditional banks and credit unions rarely offer no doc options.

Examples of no doc or low documentation lenders include:

- Bluevine – Offers lines of credit with minimal paperwork for qualified borrowers

- Fundbox – Provides revenue-based credit lines using business bank data

- Credibly – Offers working capital loans with streamlined approvals

- OnDeck – Known for fast term loans and daily repayment structures

- PayPal Working Capital – Available to PayPal sellers based on account performance

- Square Loans – Merchant-based financing tied to Square sales volume

Most of these lenders use alternative data like bank transactions, sales platform integrations or POS history to make decisions without requiring full financial statements.

Types of no doc business loans

No doc business financing comes in a few different forms. Each uses different repayment structures and underwriting criteria, but all share a streamlined documentation process.

- Merchant cash advances: An upfront sum repaid through a percentage of daily card sales. High fees, flexible repayments.

- Revenue-based financing: Monthly payments tied to gross revenue. Easier to qualify, but expensive.

- Business lines of credit: Can be offered with minimal docs if backed by strong revenue or a personal guarantee.

- Invoice financing: Borrow against outstanding invoices. No credit check or tax returns needed.

- Short-term working capital loan: Fixed-fee financing for three to 18 months, often with daily or weekly repayment.

- eCommerce platform loans: Funding based on platform performance (e.g., Amazon, Shopify, PayPal, Square), with no tax returns required.

Average Business Loan APRs as of June 2025

| Traditional Bank Loan | 6.13% – 12.36% | Established businesses with strong credit |

| SBA 7(a) Loan | 10.5% – 15.5% | Government-backed loans for various purposes |

| Online Term Loan | 14% – 99% | Faster funding, less stringent requirements |

| Merchant Cash Advance | 40% – 350% (factor rate) | Quick access based on future sales |

Must read

Since no doc loans cover several types of financing options, you can generally expect to pay a higher rate compared to traditional business loans.

Calculate the cost of your no doc business loan

Overview of your loan

Total interest / fees payable:

How lenders assess risk without documents

Lenders use alternative underwriting methods when documents are limited. These may include:

- Bank account history (average balance, deposits, withdrawals)

- Business revenue trends from accounting software

- POS system data or eCommerce platform integrations

- Collateral, such as inventory or equipment

What to watch for

No doc loans can become costly quickly, especially if repayment is daily or based on fluctuating sales. Evaluate the total cost of capital, not just interest rates. Some lenders use factor rates, which mask true APRs. Others may include fees for early repayment, origination or account maintenance.

Check the fine print on:

- Repayment frequency and method

- Total payback amount, not just interest

- Any required personal guarantee or lien

Real-world experiences with no doc business loans

Business owners shared their unfiltered experiences with no doc loans with us. Here’s what they had to say in their own words:

- Chris Bajda, Managing Partner, Groomsday:

“No doc loans were a perfect fit for us because they allowed us to quickly scale up inventory during the busy wedding season without waiting for extensive paperwork approval.” - John Beaver, Founder, Desky:

“Things ran smoothly in the beginning… Even so, there were some challenges, mainly because of the high interest rates. Their prices were higher than what I thought, and this made things cost more over the years.” - Brian Quigley, Founder, Beacon Lending:

“The good part was speed… The downside was the cost. These loans come with higher interest rates and tighter repayment terms, so you really have to run the numbers and be confident in your ROI.”

But he also mentioned, “Some lenders weren’t great with communication, so it’s easy to miss fine print if you’re not careful.” - Sreerag P, Digital Marketing Specialist, Acodez IT Solutions:

“The process itself was fast and refreshingly simple, but not without its eyebrow-raising moments — like when the repayment terms made me triple-check that I wasn’t signing away my weekends too.”

He also warned, “You need to watch out for vague terms, surprise fees and repayment models that can drain your cash flow if you’re not prepared.” - Ray Lauzums, CEO, Poggers.com:

“The big upside was speed — I got approved and funded within 48 hours with minimal documentation. But the trade-off was high costs and tight repayment terms, often daily or weekly, which can squeeze cash flow if you’re not prepared.”

Compare business loans

Weigh your business loan options by amount and requirements to see which fits your needs best. Tap Go to site to get started on your application. Or, visit our review page by choosing More info.

Compare other products

We currently don’t have that product, but here are others to consider:

How we picked these

What is the Finder Score?

The Finder Score crunches 12+ types of business loans across 35+ lenders. It takes into account the product’s interest rate, fees and features, as well as the type of loan eg investor, variable, fixed rate – this gives you a simple score out of 10.

To provide a Score, we compare like-for-like loans. So if you’re comparing the best business loans for startups loans, you can see how each business loan stacks up against other business loans with the same borrower type, rate type and repayment type.

Read the full Finder Score breakdown

Alternatives worth considering

If you can afford to wait, a traditional business loan or SBA microloan may be more affordable long-term. Other flexible options include:

Bottom line

No doc business loans offer a fast, flexible option for entrepreneurs with documentation gaps or urgent cash needs. But that convenience comes at a premium. If you can produce even basic financials, better terms may be available elsewhere. For time-sensitive situations or newer businesses, no doc loans can be a practical bridge, so long as repayment obligations are clearly understood.

FAQs

Are no doc business loans truly documentation-free?

No. While they don’t require full financial statements or tax returns, lenders still need to assess risk. Most will ask for bank statements, proof of revenue, or basic business details.

How fast can I get funding with a no doc loan?

Funding can happen in as little as 24 to 72 hours, depending on the lender and the information you provide. Speed depends on how quickly you can verify your revenue or bank activity.

Do no doc loans affect my credit score?

Yes, many lenders report loan activity to credit bureaus. Some may do a soft pull during prequalification, but a hard credit inquiry usually occurs before final approval.

Can startups qualify for no doc business loans?

Yes, especially if they have strong bank activity or collateral. Some lenders specifically market to new businesses or sole proprietors with limited documentation.

Can I get a no doc business loan with an EIN only?

Yes, but it’s rare. Most lenders require more than just an EIN (Employer Identification Number) to approve a no doc business loan. While an EIN is necessary to identify your business, lenders typically also want to see recent bank statements, proof of revenue, or access to your sales platform. Some fintech lenders may approve small loan amounts based primarily on business activity tied to your EIN, but expect to provide additional data like:

- Business checking account history

- Time in operation (usually 3–6 months minimum)

- Online sales or payment processor activity (e.g., Shopify, Stripe, Square)

No doc loans that accept EIN-only applications are typically secured with daily repayments, higher interest costs and may require a personal guarantee even if your Social Security number isn’t used up front.